Tax On Income From House Property | Saving Taxes On House Property

For income to be charged under the head house property it generally requires two conditions i.e. ownership and a building, if you are having a building and own it then you can charge your income under Income From House Property whether self occupied or let out. The thing to be noted here is ownership includes beneficial ownership as well while calculating Tax On House Property.

Your house property income gets added to your total income and is taxed as per normal slab, thereby giving lot of scope for reducing tax on house property income through various deduction and exemption benefits. Though expenses to your property such as repairs, renovations are not explicitly allowable from your income but nevertheless income tax laws have provided with various tax benefits for your house property tax income.

Prerequisites for charging House Property Income

- Building or land appurtenant thereto

(Other than such portion used by him for carrying business)

- Ownership

Including deemed ownership which includes

- Transfer of ownership to a spouse (other than as consideration to live apart) or minor child (other than minor married daughter)

- Holder of impartible estate.

- Property held by member of a co-operative society

- Any person who has acquired a property under Power of Attorney transaction.

Computation for House Property Income

Determination of Annual value

Let out House property

Gross Annual value is higher of

- Expected rent – higher of Municipal value and fair rental value

- Actual rent received or receivable for the period it remained occupied

Self occupied house property

Annual value – Nil

What is self occupied?

Property which –

- is in the occupation of the owner for the purposes of his own residence; or

- cannot be occupied owing to his employment, business or profession carried on at any other place, and owing to which he has to reside at other building not belonging to him,

If assessee has more than one self occupied house property than he has to declare one as self occupied and the other will be deemed to be let out.

Municipal taxes

Taxes paid to municipality and local authority can be deducted from the Gross Annual Value of property in the year when it is paid, it should be noted that, it is allowable only if it is paid by owner, taxes paid by tenants is not allowable, it is also worthy to note that tax should have been actually paid and not merely payable.

Computation

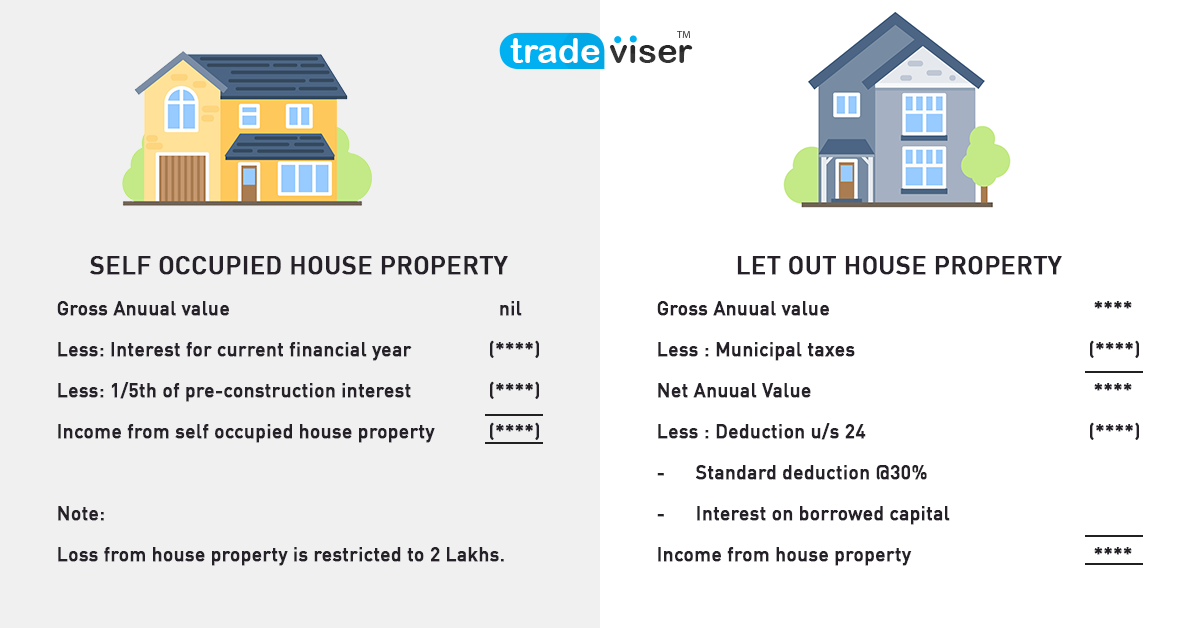

| Self occupied House Property | |

| Gross Annual value | **** |

| Less: Interest for current financial year | **** |

| Less: 1/5th of pre-construction interest | **** |

| Income from self occupied house property | **** |

| Let out House Property | |

| Gross Annual Value | **** |

| Less : Municipal taxes | **** |

| Net Annual Value | **** |

| Less : Deduction u/s 24 | **** |

| – Standard deduction @30% | **** |

| – Interest on borrowed capital | **** |

| Income from house property | **** |

Computation of Tax on House Property Income

Exemptions, deductions and how to save income tax on house property

Implications on set-off and carry forward of loss: Loss from IFHP cannot be set-off against other heads of income exceeding Rs.200,000. The amount which is not set-off however can be set-off against future 8 Assessment years.

Deductions from income from house property.

Standard deduction @ 30%

- Interest on loan taken for the purpose of house property i.e. for Construction, repairs and renovation is deductible against your rental income, the quantum of deduction depends upon whether your house property is self occupied or let out.

If you are paying interest for house property which is let out then there is no limit on the interest deduction, but it is not the same with self occupied property, wherein if the loan is taken on or after 1.4.1999 for purchase or construction of house property the deduction would be restricted to maximum of Rs.2,00,000 ,while in other cases it is Rs 30,000.

Special points for construction

- The said higher limit of Rs.2,00,000 in case of self occupied property is applicable only if construction is completed within 5 years from the end of the year in which loan was taken.

- Any interest paid in pre-construction period is allowable in 5 equal installments from the end of the year in which construction is completed.

Other points

- Interest on any fresh loan taken for repayment of earlier loan which was taken for the purchase of house property shall also be allowable as deduction. (circular No. 28 dated 20th August 1969)

- Interest if paid outside India will be allowable only if TDS is been deducted on the same.

- It is worth noting that loan can be taken from any person and not only banks and financial institutions

Deduction under Section Section 80EE

It is another way to save your tax on house property, though it is not directly subtracted from your house property income but is subtracted from your taxable income. Amount of interest over and above section 24 can be claimed under section 80EE up to Rs.50,000 per financial year.

However it is subject to certain conditions

- The property should be first house of the assessee

- House value should be Rs. 50 lakhs or less.

- The loan should be Rs. 35 lakhs or less.

- Deduction is only for the interest portion.

- The loan should be sanctioned by a Housing Finance Company or a Financial Institution.

- As on the date of the loan sanction, the individual must not own another house.

- The loan should not have been availed for commercial purpose.

- The loan should be sanctioned between 01.04.16 to 31.03.17.

Example: Mr. X paid interest of Rs.2,30,000 towards loan which was acquired for house property. Assuming it is self occupied house property he can claim Rs.2,00,000 under section 24 and Rs. 30,000 under Section 80EE subject to fulfillment of other conditions.

FAQs

- My daughter stays in USA. She owns a house in India and has let it out. She has asked tenants to pay rent to me. She has not received any rent. Is she still liable to tax? What if she transfers the house to me?

Rental income is charged to tax in the hands of the owner of the property. Your daughter is the owner of the house and, therefore, she is liable to pay tax, even though you receive rent. If the house is transferred to you, then you will become the owner and you will have to pay Income-tax on the rental income.

- What is unrealized rent? What is its treatment?

the amount of rent which the owner cannot realise shall be equal to the amount of rent payable but not paid by a tenant of the assessee and so proved to be lost and irrecoverable.

It is subtracted from your Annual value

Click here for your free Tax Consultation

Reshma Jain (born Chennai, 1995) is a Qualified Chartered Accountant by profession and has a Bachelor’s degree of Commerce. Has practical knowledge of tax, company law, and auditing. Believes in a simple approach to creative writing and learning.